Those are the questions that matter.

The Better Approach: Be Pro-Plan

Being reflexively anti-annuity can cause an advisor to miss a useful planning tool. Being reflexively pro-annuity can lead to product-driven advice. Neither approach is ideal.

The better approach is to be pro-plan.

Annuities deserve neither blanket endorsement nor blanket criticism. They should be evaluated the same way any financial tool should be evaluated: by asking what role they play, what risk they are intended to address, what trade-offs they require, and whether those trade-offs are worth it for that specific client.

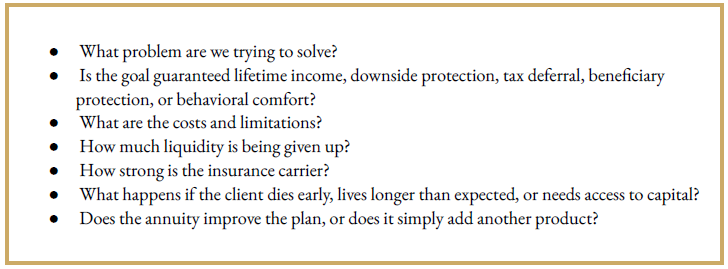

How Revant Evaluates Financial Tools

An annuity is not a financial plan. But in the right situation, it may play a valuable role inside one.

At Revant, this is the lens we bring to conversations around annuities and any other financial tool. The product is never the starting point. The plan is. Before any recommendation is made, the purpose has to be clear, the trade-offs have to be understood, and the strategy has to fit within the client’s broader financial life.

The product should serve the plan. The plan should never be built around the product.

This material is for general information and educational purposes only and is not intended to provide specific advice or recommendations for any individual. Investing involves risk including the loss of principal. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes.

Revant Wealth and LPL Financial do not provide legal advice or tax services. Please consult your legal advisor or tax advisor regarding your specific situation.

Annuities are long term, tax-deferred investment vehicles designed for retirement purposes and contain both an investment and insurance component. They have fees and charges, including mortality and expense risk charges, administrative fees, and contract fees. They are sold only by prospectus. Guarantees are based on the claims paying ability of the issuer. Withdrawals made prior to age 59 ½ are subject to 10% IRS penalty tax and surrender charges may apply. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. The investment returns and principal value of the available sub-account portfolios will fluctuate so that the value of an investor’s unit, when redeemed, may be worth more or less than their original value.